Editorial Note: We earn a commission from partner links on Doughroller. Commissions do not affect our authors’ or editors’ opinions or evaluations. Learn more here.

Empower and Wealthfront are two of the most popular investment managers. And while they have similar investment platforms, each caters to a very different clientele. Empower is oriented toward those who are looking for traditional human investment management, but at a lower fee. It also offers a substantial amount of budgeting and personal finance management assistance.

Wealthfront, by contrast, targets the general investment public and will be more appealing to a larger number of investors. Their fees are substantially lower than Empowers, as is their minimum initial investment. It’s a perfect investment platform for a new or small investor, who is looking for comprehensive investment management at a very low cost.

About Empower and Wealthfront

Empower

Empower is primarily a fee-based wealth management platform, but it also offers free financial software for budgeting and personal finance management. The free financial software is quite comprehensive, and also offers extensive investment tools. You can use the free financial software in conjunction with wealth management, or you can just use the software itself. The service is currently being used by more than 1.6 million people.

Wealthfront

Weathfront is an automated investment service, more commonly known as a robo-advisor. You put your money into the account, and all aspects of investment management are handled for you. That includes portfolio selection, rebalancing, dividend reinvestment, and tax minimization.

You complete a brief questionnaire to determine your risk tolerance, goals and time horizon, then Wealthfront builds your portfolio. They do this by investing in a minimum of seven different asset classes (to as many as 11).

Unlike Empower, Wealthfront doesn’t offer budgeting or personal finance software, though they do offer tools to help you reach different financial goals.

Investment Management

Empower Wealth Management

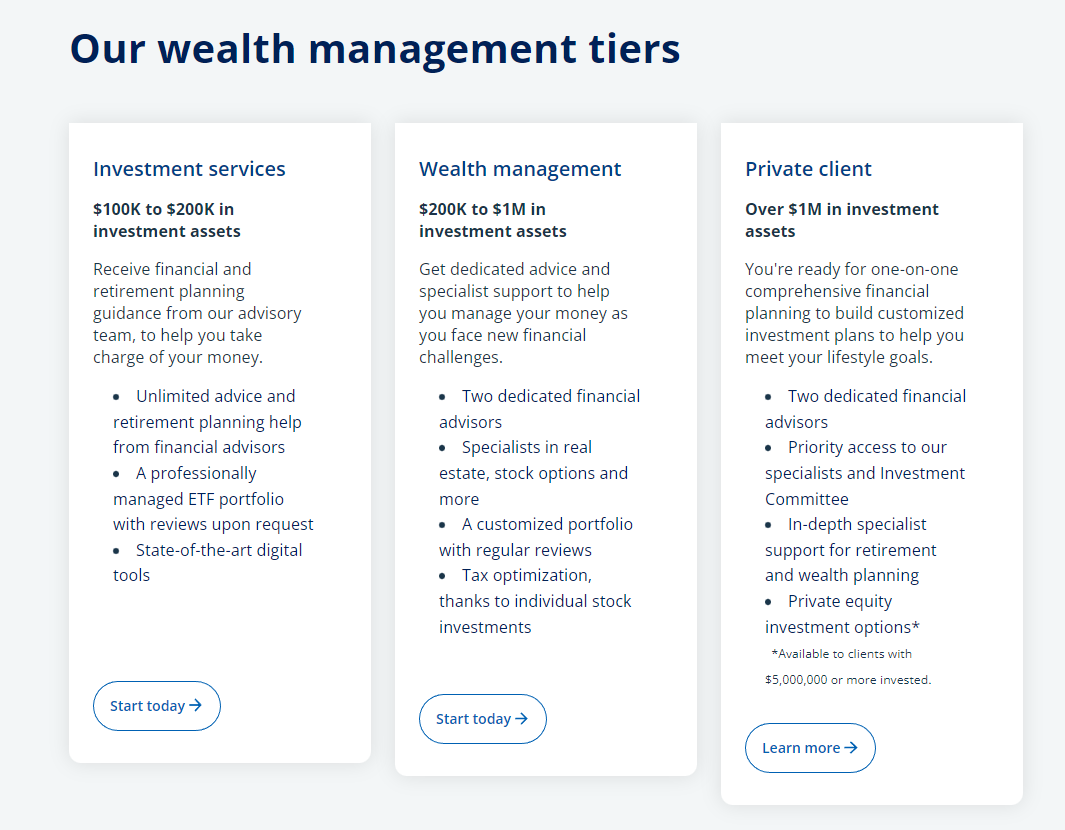

Empower offers three different investment management services:

- Investment Services for up to $200,000 in investable assets

- Wealth Management for $200,000 to $1 million in investable assets

- Private Client for over $1 million in investable assets

The screenshot below breaks down the service levels for each plan. As you can see, when you move into Wealth Management and Private Client, you’re not just looking at investment management but also full financial planning services.

Empower Investment Methodology

Empower uses a tactical weighting approach with traditional indexing of U.S. equities. They do this by maintaining more evenly weighted exposure to every sector and stock. Back tests have indicated this methodology has outperformed the S&P 500 by more than 1.5% per year, and did so with lower volatility. They generally favor passive investing.

Your investment strategy will be customized, based on your overall financial situation and your personal goals. They will incorporate medium-term investment goals, like financing a college education or buying a home.

Investment mix -Your portfolio will be constructed based on Modern Portfolio Theory (MPT). Equities will include a well-diversified sample of 90 to 120 individual stocks (mega-, large- and mid-cap) for both tactical weighing and tax optimization, as well as small-cap index ETFs. On the fixed-income side, they use a combination of low-cost exchange-traded fund (ETFs).

Asset classes used in your portfolio include:

- U.S. Stocks

- International Stocks

- U.S. Bonds

- International Bonds

- Alternatives including hard assets, like real estate investment trusts (REITs), gold and energy, as hedges against inflation

- Cash, for liquidity

Investment custodian– Empower doesn’t require you to deposit your investment funds with them. Instead, your account is held with Pershing Advisor Solutions, a Bank of New York Mellon company. Pershing holds more than $1 trillion in global client assets. You can view your various accounts through the Pershing online platform, which can be accessed from the Empower dashboard. You will also receive periodic electronic statements from both Pershing and Empower.

Portfolio rebalancing– Your portfolio is monitored daily, and rebalanced as necessary to keep asset classes within target allocations.

Other Empower Investment Features and Benefits

Minimum initial investment– $100,000 for the investment management version, but no minimum for the free financial software.

Accounts available– Individual and joint taxable accounts; traditional, Roth, rollover and SEP IRAs; and Trusts. Advice only (no direct management) provided on employer-sponsored retirement plans, and 529 college plans.

Access to financial advisors– Empower gives you access to financial advisors on the paid version. If you have at least $200,000 being managed, you’ll have two dedicated financial advisors.

Tax minimization– Empower uses various strategies to minimize investment generated income taxes. These include tax-loss harvesting and tax allocation. Tax allocation involves holding income generating assets in tax-sheltered accounts, while capital gains generating assets are held in taxable accounts to take advantage of more favorable long-term capital gains rates. They also use various tax efficiency strategies, including avoiding mutual funds, since they are more likely to generate capital gains.

Socially Responsible Investing (SRI)– Empower has recently rolled out SRI to invest in companies that are doing the most good for the environment, society and corporate governance. They invest in the same six asset classes listed earlier, but with a strong orientation in favor of social responsibility. They also avoid certain sectors, including adult entertainment, gambling, tobacco, controversial weapons, military contract, and small arms.

Wealthfront

Wealthfront offers its base service to investors at all account levels. They also offer certain enhanced investment options for larger investors.

Wealthfront Investment Methodology

Wealthfront also makes use of modern portfolio theory. They generally follow a passive investing strategy, which involves matching underlying investment benchmarks, rather than trying to outperform them. They do this by investing your portfolio in low-cost, index-based ETFs.

Asset classes– Wealthfront spreads your portfolio across as many as 11 different asset classes:

- U.S. Stocks

- Foreign Developed Market Stocks

- Emerging Market Stocks

- Dividend Growth Stocks

- U.S. Government Bonds

- Corporate Bonds

- Emerging Market Bonds

- Municipal Bonds (taxable accounts only)

- U.S. Treasury Inflation-Protected Securities (TIPS)

- Real Estate (through a real estate investment trust)

- Natural Resources

A corresponding ETF is used for each asset class. Exactly which asset classes your portfolio will be invested in, and what the specific allocation will be, depends on your investor profile (goals, time horizon and risk tolerance).

Wealthfront provides both periodic rebalancing and automatic dividend reinvestment on all accounts.

PassivePlus– This is a strategy Wealthfront offers designed to increase returns without increasing portfolio risk. They use time-tested, rules-based strategies to invest beyond index funds. PassivePlus incorporates smart beta (see next section).

Wealthfronts historical returns, through June 30, 2018, are as follows (based on a risk score of 8.0, on a scale of 0.5 to 10.0):

Other Wealthfront Investment Features and Benefits

Minimum initial investment– $500

Accounts available– Individual and joint taxable accounts; traditional, Roth, rollover, and SEP IRAs; trusts and 529 college savings plans.

Tailored Transfers– With Wealthfront, transfers will be accomplished gradually to minimize the tax implications, rather than immediate liquidation to cash. However, they will recommend you sell incompatible investments, like mutual funds since they don’t fit within Wealthfront’s investment methodology.

Tax minimization– Wealthfront offers tax-loss harvesting on all accounts. They also optimize tax outcomes through tax location, again holding income generating assets primarily in tax-sheltered plans, with capital gains generating assets in taxable accounts. They make use of index funds to minimize capital gains resulting from active trading in mutual funds. Wealthfront also uses dividend reinvesting to rebalance your portfolio, once again minimizing capital transactions.

Risk Parity Fund– This is a mutual fund offered by Wealthfront, and available to account holders with balances of at least $100,000, and for taxable accounts only. Risk parity works to increase your risk-adjusted returns in a wide range of market environments through enhanced asset allocation strategy. Using the same asset allocations in the basic portfolio, it allocates them in a different way. It is believed the fund can provide higher absolute and risk-adjusted returns.

Smart Beta– This service is available at no additional cost to investors with a minimum of $500,000. Smart beta increases your returns by weighing individual securities in your portfolio more intelligently. As a bonus, Smart Beta is offered with stock level tax loss harvesting.

Socially Responsible Investing (SRI)– Wealthfront offers this in a modified form. SRI is supported through smart beta and stock level tax loss harvesting. If you qualify for either, you can let them know which companies you do not wish to invest in.

Features Unique to Each Platform

Empower

Empower is primarily a wealth management service. But it does offer its free financial software. It provides budgeting, and even investment applications.

Features included in the free version include:

- Budgeting

- Goal setting, including strategies to help you reach your goals

- Managing your investments

- Planning and managing your retirement accounts

- Creation of income and spending reports, as well as upcoming bills

You can assemble all your financial accounts on the Empower platform. That includes bank accounts, investments, retirement accounts, credit cards, mortgages and other loans. You can also track the most important number in your financial picture–your net worth. Knowing this enables you to compare your net worth to the median U.S. household net worth for your age bracket.

As budgeting software goes, it’s not as comprehensive as some other platforms. For example, it doesn’t offer a Bill Pay service, nor does it enable you to reconcile accounts or transactions. The budgeting service is mainly a good feature to have, in addition to the investment capability.

Interesting features offered in the free version include:

Investment Checkup tool– Analyzes your portfolio and recommends improvements to help you reach your goals. They’ll also recommend a portfolio to improve your investment performance.

Fee Analyzer– Helps identify hidden investment fees, and recommends alternative investments to cut those fees, improving your long-term investment performance.

Retirement Planner– This feature offers several different retirement related tools, including the Retirement Calculator. Track your progress against your retirement goals, and make adjustments where needed. You can even calculate projected Social Security benefits, as well as pensions and rental income.

The Retirement Planner can even be used for non-retirement expenses, like saving for a down payment on a home or an upcoming wedding, or budgeting for your child’s college education.

Crypto Tracker – Empower recently added the ability to link and monitor your cryptocurrency right within the dashboard. After seeing their users link 28% more assets to their dashboards in 2020, plus the rush on crypto investing, it made sense to give users this ability – and it’s a game-changer. Now you can track thousands of different tokens from hundreds of exchanges to see your balances and individual crypto values.

Wealthfront

Once again, Wealthfront doesn’t offer budgeting, but they do offer tools and features you won’t find with Empower.

Portfolio Line of Credit– You can borrow against your Wealthfront investment account with no application, no fee, and no credit check. Since it is a secured line, interest rates currently range between 2.40% and 3.65% APR depending on account size, which is comparable to home equity lines of credit. You need an investment account balance of $25,000 or more to be eligible. You can borrow up to 25% of your account balance at any time, and for any purpose. You can then repay it on your own schedule.

Wealthfront Path

Wealthfront has a tool called Path that helps you plan and track your major financial objectives in life.

Homebuying– The tool can help you to find the right home for your budget. It’s integrated with the online real estate platform, Redfin, providing you with real-time prices to fit within your budget. It will help you to get a mortgage amount based on your location, net worth, credit score and debt-to-income ratio. It adds in property taxes, insurance and maintenance with your payment, and even factors in closing costs.

Retirement– Path calculates your future retirement based on changes in your circumstances. This can include a promotion at work, a new addition to your family, or the purchase of a home. You link your various financial accounts to Path, and it will analyze your financial habits. They use a team of PhDs to help forecast economic factors like inflation and Social Security, to give you a comprehensive view of your retirement situation. You can also make changes along the way, that might enable you to retire early. You’ll then be told how much to invest and which accounts will best accomplish your goals.

College savings. Path analyzes the total college picture, including how much it will cost, financial aid available, and how much you’ll need to and save and invest. You can either open a new 529 college savings plan with Wealthfront, or link an existing plan from another sponsor.

Wealthfront Cash

Wealthfront Cash is a relatively new addition to the Wealthfront lineup, and it acts like a savings account. You can store cash there for an emergency or future purchase, just as you would with a savings account, or you can keep uninvested cash in the account until you’re ready to use it.

Currently, you will earn [ct_brand_render field=ctsavings_interest_rate id=128001051 /] APY on the Wealthfront Cash account–which isn’t much, but better than regular savings account yields right now–and it has a few other benefits you will like.

First, it’s FDIC-insured up to $5 million, but what’s even better is that you can make as many withdrawals as you want during the month without paying a fee–this is because it doesn’t have the same regulations as a savings account. There are also no fees, it only takes $1 to set up, and JUST launched is the ability to direct deposit your paycheck and have a debit card through the new checking feature.

That’s right – Wealthfront cash accounts now have a checking feature, where you can get a debit card for purchases, pay your bills online, and have your paycheck deposited right into the account. You can also deposit paper checks with the mobile app, pay others through apps like Venmo, and even get paid up to two days early when you have direct deposit set up.

Read more: Wealthfront Cash Account full review

Pricing

Empower Pricing and Plans

As we’ve already reported, Empowers financial software is available to anyone free of charge. That includes not only the budgeting capabilities but also the investment support services.

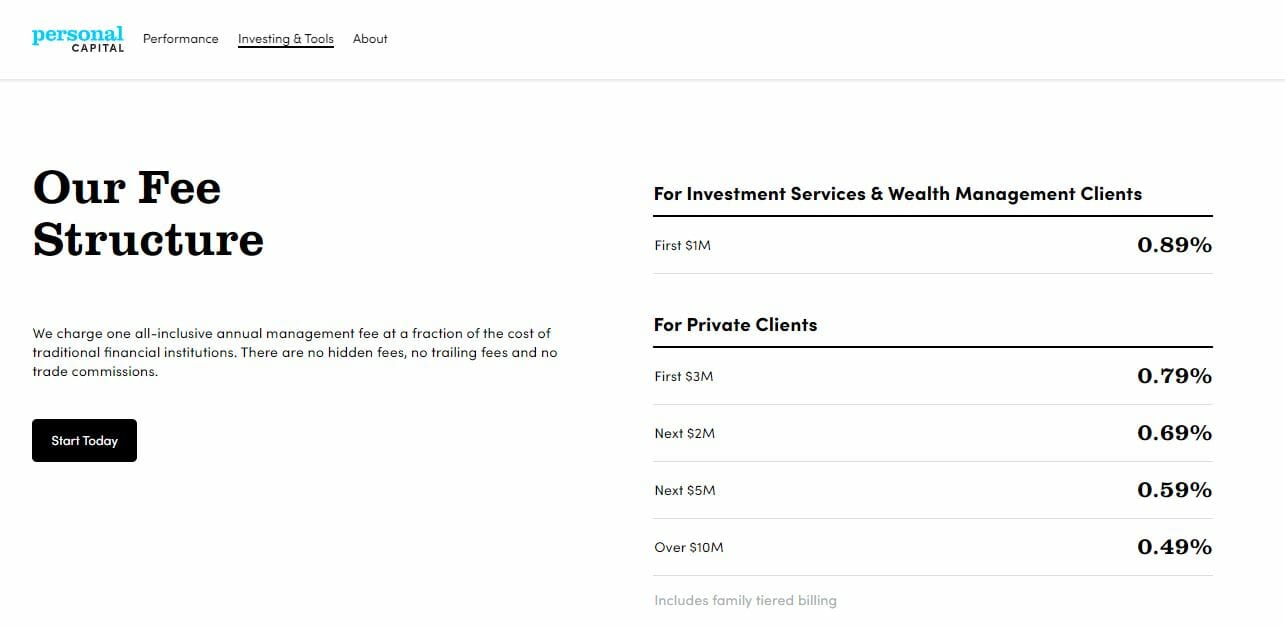

The Wealth Management versions use a tiered advisory fee. It can be as low as 0.49% per year for very large account balances, but most investors will pay 0.89%. The fee applies only to actual investments under management with Empower. For example, if you include employer-sponsored retirement plans, the fee won’t apply to those balances even though Empower may make investment recommendations for those accounts.

The complete Wealth Management fee structure is as follows:

Wealthfront Pricing and Plans

Wealthfront charges a flat annual advisory fee of 0.25%. That means you can have a $10,000 account managed for $25 per year, or a $100,000 portfolio for $250 per year. This fee is at the lower end of the robo-advisor industry range. There are no additional fees, such as trading commissions.

Wealthfront also discloses that the expense ratio of the ETFs they use is 0.09% per year. These are fees charged within the ETFs used, and not direct charges from Wealthfront to you as an investor.

Customer Service

Empower Customer Service

Empower offers contact by phone or email 24 hours a day, seven days per week. They also offer a comprehensive FAQ page, which is focused mostly on Wealth Management. They also provide a Support Portal providing a large amount of information on the free financial software.

Wealthfront Customer Service

Wealthfront Customer Service can be reached by either phone or email, Monday through Friday, 7:00 AM to 5:00 PM, Pacific time. They also offer a Help Center page where you can get answers to questions on a variety of topics, and receive immediate information.

Wealthfronts Learning Center provides articles and videos on a wide range of topics, including IRAs, 529 plans, 401(k) plans, and general investing.

Accessibility

Empower

Empower is available for desktop, tablet and mobile devices. The mobile app is available for iOS and Android devices, as well as Apple Watch, and can be downloaded at the App Store or on Google Play.

Wealthfront

Wealthfront is available for desktop, tablet and mobile devices, including iOS and Android devices.

Promotions

Wealthfront Promotions

The first $5,000 invested with Wealthfront is managed for free for DoughRoller readers.

Bottom Line

Empower is designed primarily for larger investors, looking for full-service investment management. They compete less with robo-advisors like Wealthfront, and more with traditional human investment management. In that regard, they offer much lower fees than the usual 1.00% to 1.50% charged by traditional investment managers.

They offer comprehensive wealth management, including socially responsible investing, a tactical weighing investment approach, and tax minimization strategies. And of course, they also offer their free financial management software, that helps you with budgeting and the management of your overall financial situation.

Read More: Empower Alternatives

Where Empower falls short is that it doesn’t work as an investment solution for small investors. First, the account minimum of $100,000 excludes small investors. Then the annual advisory fee starting at 0.89% is well above what small investors can get through robo-advisors, including Wealthfront.

Wealthfront is a true robo-advisor, and is in fact one of the largest independent robo-advisors in the industry. They offer comprehensive investment management at a very low fee. And since they require an account minimum of just $500, it’s very well-suited to new and small investors.

Related: The Best Robo Advisors

Wealthfront does offer advanced investment options for larger portfolios. But it does not come with the one-on-one financial advice offered by Empower. And while it offers customer service to all participants, it is first and foremost an automated investment service, and doesn’t provide direct, personal investment advice.

Empower’s free financial tools are must-try for everyone while their Wealth Management service is best used for larger investors looking for comprehensive investment and financial management. Wealthfront is the perfect investment platform for new and small investors, who are looking for complete investment management at a low fee, and with a very small initial investment.